[New post] Fed rate increase gives another boost to savings accounts

gqlshare posted: "It's 2023 and the Federal Reserve just announced a federal funds rate range increase of 0.25%. This is after seven rate increases in 2022. This increase brings the target funds rate range up to 4.5%-4.75%. This increase is smaller than some of the s" Colorado Daily

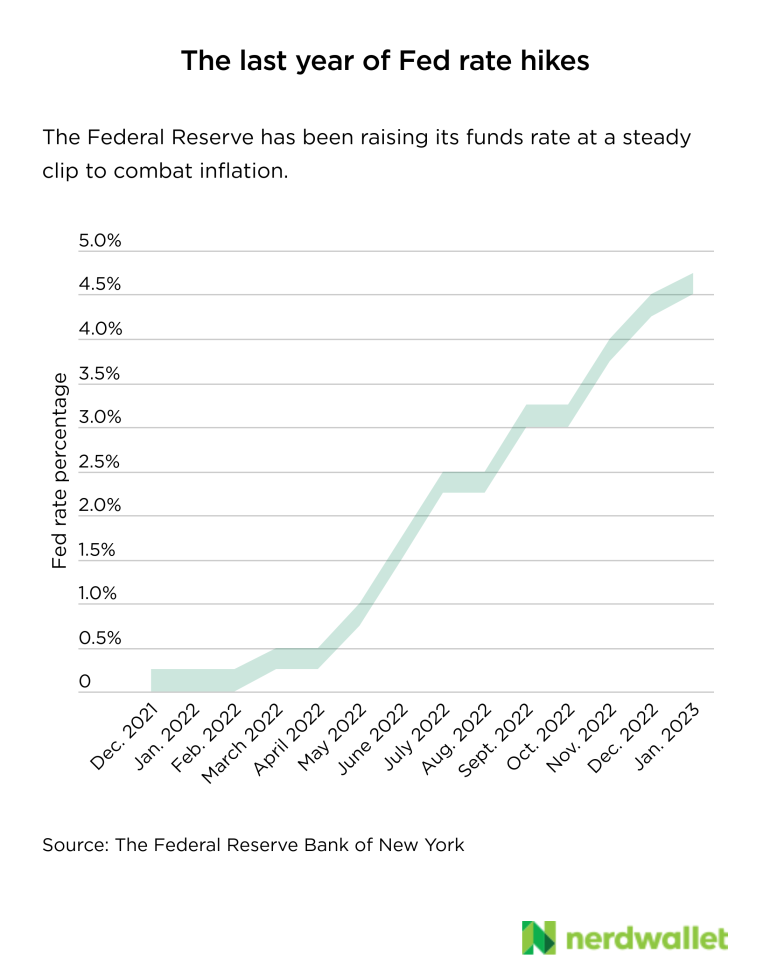

It's 2023 and the Federal Reserve just announced a federal funds rate range increase of 0.25%. This is after seven rate increases in 2022. This increase brings the target funds rate range up to 4.5%-4.75%. This increase is smaller than some of the steep changes in 2022, but another increase means rates are at their highest point since 2007, which was the last time the target hit 4.75%.

All of the recent rate increases mean loans and credit card balances are more expensive. But if you have a savings account or certificate of deposit, you could benefit. Here's a look at what the latest rate increase could mean for savings accounts in 2023.

Savings accounts: 3% APY or higher

In early 2022, some of the best savings accounts earned a mere 0.50% annual percentage yield. Today, the best savings accounts earn more than 3% APY, and a few of the top high-yield savings accounts are at 4% APY.

That's a large jump for one year. Since the most recent Federal Reserve announcement states a smaller increase compared to most of the 2022 rate bumps, don't expect to see APYs that are nearly eight times higher. However, you may still see yields that edge a little higher, and more accounts may reach the 4% figure.

Keep an eye out for high-yield online savings accounts in particular, which tend to offer some of the highest rates.

On the other hand, savings accounts in a few of the largest national banks have rates that are 0.01%, despite the multiple federal fund rate increases last year. These rates lag behind the national average savings rate, which is 0.33% as of January 17, 2023, according to the Federal Deposit Insurance Corp.

If you have a savings account with a subpar rate, it could be worth your effort to shop around for a savings account that earns 3%-4% APY.

Shore up savings for the future

One of the reasons the Federal Reserve has been increasing rates is that it wants to fight inflation. Efforts from last year seem to be working. According to the U.S. Bureau of Labor Statistics, the consumer price index, which is often used as a measure of inflation, increased 6.5% year over year in December 2022. That figure, while relatively high compared to previous years, is lower than it was earlier that summer, when the CPI was 9.1% year over year in June 2022. If inflation falls within the Federal Reserve target range in the coming months, rate increases may end.

That's all the more reason to build up an emergency fund in a high-yield account now. No one can predict the future, but having a strong savings account can help prepare you to weather a financial storm.

It's ideal to have three to six months' worth of your expenses in savings, but that's a lot. If you don't have that much saved up just yet, you can build it up over time in amounts that are feasible for you.

Say you receive a paycheck twice a month and are able to put away $50 each payday. You'll have more than $600 saved up within six months, and that can help in a financial emergency. Putting that cash in an account with a high rate can help you grow your funds.

The difference a high-yield savings account makes

Where you keep your savings can have an effect on your balance. If you put your emergency fund of $600 in an account with a 0.01% APY like that offered by many of the largest national banks, and you didn't make any additional deposits, it would earn a total of only 6 cents after a year. But if that money was in a high-yield savings account that earns a 4.00% APY, even if you didn't make any additional deposits, the balance would grow by more than $24 in that same time period. That's a gain for simply choosing a better savings account.

You can try your own calculations with NerdWallet's savings calculator to see what your savings could earn.

Fed rate increases are continuing into 2023 — so far. Take advantage by storing your money in a high-yield savings account. You'll earn better rates than with a regular savings account, and you can be better prepared for whatever financial situations come your way.

No comments:

Post a Comment